Chapter 35 — Different Market Structures

Cambridge International AS & A Level Economics (9708) · Unit 8.1 · 4th edition coursebook

Learning objectives

- Describe the market structures of perfect competition and imperfect competition (monopoly, monopolistic competition, oligopoly and natural monopoly).

- Explain the characteristics of the market structures in terms of the number of buyers and sellers, product differentiation, degree of freedom of entry and availability of information.

- Explain barriers to entry and exit (legal, market, cost, physical).

- Analyse the performance of firms in different market structures through revenues and revenue curves, output in the short run and in the long run, profits in the short run and in the long run, shutdown price in the short run and in the long run, deriving a firm's supply curve in a perfectly competitive market, efficiency and X-inefficiency in the short run and in the long run, price competition and non-price competition, collusion and the Prisoner's Dilemma in oligopolistic markets (including a two-player pay-off matrix).

- Define the meaning of a concentration ratio.

- Calculate a concentration ratio.

- Analyse the features and implications of contestable markets.

Key terms

- market structure

- The way in which a market is organised in terms of certain characteristics which can be used to explain the behaviour of firms in a market.

- perfect competition

- An ideal market structure that has many buyers and sellers, identical products, no barriers to entry; sometimes referred to as total competition.

- imperfect competition

- Any market structure except for perfect competition.

- monopolistic competition

- A market structure where there are many firms, differentiated products and few barriers to entry.

- oligopoly

- A market structure with few firms and high barriers to entry.

- barriers to entry

- Restrictions that prevent new firms entering an industry.

- pure monopoly

- Where there is just one seller in the market.

- natural monopoly

- Where with falling long-run average costs, it makes sense to have only one firm providing the good or service.

- concentration ratio

- A measure of the combined market share of the biggest three, four or five firms in a market.

- predatory pricing

- Where a firm sells its goods below average variable cost to force competitors out of the market.

- limit pricing

- Where firms deliberately lower prices and abandon a policy of profit maximisation to stop new firms entering a market.

- collusion

- An anti-competitive action by producers.

- barrier to exit

- A restriction that prevents a firm leaving a market.

- shut-down price

- A firm will stop production when price falls below average variable cost.

- price competition

- Where firms compete on price to attract customers.

- non-price competition

- When firms use methods other than price to attract customers from rival producers.

- kinked demand curve

- A traditional model of a firm's behaviour in oligopoly.

- price rigidity

- Where prices are unchanged despite a change in costs.

- price leadership

- A situation in a market whereby a particular firm has the power to change prices, the result of which is that competitors follow this lead.

- cartel

- A formal agreement between firms to limit competition by limiting output or fixing prices.

- X-inefficiency

- Where the firm's costs are above those experienced in a more competitive market.

- contestable market

- A market where entry is free and exit is costless.

- contestability

- The extent to which barriers to entry into a market are free and exit from the market is costless.

- deregulation

- When barriers to entry into an industry are removed.

35.1Market structures and their characteristics

The term market structure describes the way in which goods and services are supplied by firms in a particular market. It is identified by four key characteristics: the number of buyers and sellers, the nature of the product (whether goods are identical or differentiated), the ease of entry into the market, and the extent to which firms share the same information about prices and production techniques.

Economists work with idealised models of market structure. The value of these models is that any real-world market can be compared against them and conclusions drawn about its efficiency. The most competitive end of the spectrum is occupied by perfect competition, an ideal in which many firms produce identical products with complete freedom of entry and perfect information; every firm is a price taker. Every other structure is collectively known as imperfect competition.

The four main models

Monopolistic competition has many firms and easy entry, but each firm has slight control over price because its product is differentiated by quality, brand or some other feature. Firms are price makers within a narrow range. Oligopoly has few firms, with substantial barriers to entry that protect their position. Products can be either differentiated or undifferentiated, and firms have considerable power to set prices subject to the reactions of rivals. Pure monopoly is a single seller for the whole market; in practice, the term also covers a firm that dominates with a very large share. Barriers to entry are very high and information is limited. A natural monopoly is a special case in which long-run average costs are lowest when one firm serves the whole market.

The characteristics summarised

The four models can be compared along five characteristics: the number of firms (very many in perfect competition, many in monopolistic competition, few in oligopoly, one in monopoly); product differentiation (identical in perfect competition, differentiated in monopolistic competition, differentiated or identical in oligopoly, unique in monopoly); barriers to entry (none in perfect competition, low in monopolistic competition, high in oligopoly, very high in monopoly); the degree of control over price (price taker in perfect competition, limited in monopolistic competition, some in oligopoly, considerable in monopoly); and the availability of information (perfect in perfect competition, some in monopolistic competition and oligopoly, little in monopoly). Together these features place each market on a spectrum of competition running from perfect competition at one end to pure monopoly at the other.

A common mistake is to confuse monopoly with monopolistic competition. The two terms sound alike but describe very different structures: monopolistic competition has many firms with slight product differentiation and easy entry, while monopoly has a single dominant seller and high barriers to entry.

Identifying the structure of a real market

To place a real market on the spectrum, several practical methods can be used.

- Count the number of firms. The larger the total, the closer the market is to perfect competition.

- Calculate a concentration ratio. This measures the combined market share of the biggest three, four or five firms as a percentage of the total market. It is calculated by adding the percentage market shares of each top firm in terms of volume or revenue. The bigger the percentage, the closer the market is to the oligopoly and monopoly models. For the four-firm concentration ratio: 4-firm CR = (combined market size of top 4 firms / total market size) x 100%.

- Assess the ease of entry and exit. Substantial barriers to entry are indicative of market structures on the less competitive side of the spectrum.

- Assess the importance of economies of scale. The more important they are, the closer the market is to an oligopoly or monopoly, because large incumbents enjoy cost advantages that smaller potential entrants cannot match.

A competition road map

Picturing the four structures as a journey from one end of the spectrum to the other helps fix the relationships between them. At the start of the journey, perfect competition has many firms, no barriers to entry, no control over price and full information. Moving along into monopolistic competition, the number of firms is still large but products become differentiated, barriers are small and competitive behaviour intensifies. Crossing into oligopoly, the number of firms collapses to a few, barriers to entry rise sharply, and firms exhibit interdependence and the possibility of tacit collusion. Finally, monopoly is reached: a single firm, a lack of close substitutes, very high barriers to entry and considerable control over price. The obvious conclusion might be 'competition good, no competition bad' - this is often true, but the more careful point is that the opportunity to compete (rather than competition itself) is what drives efficiency in a market.

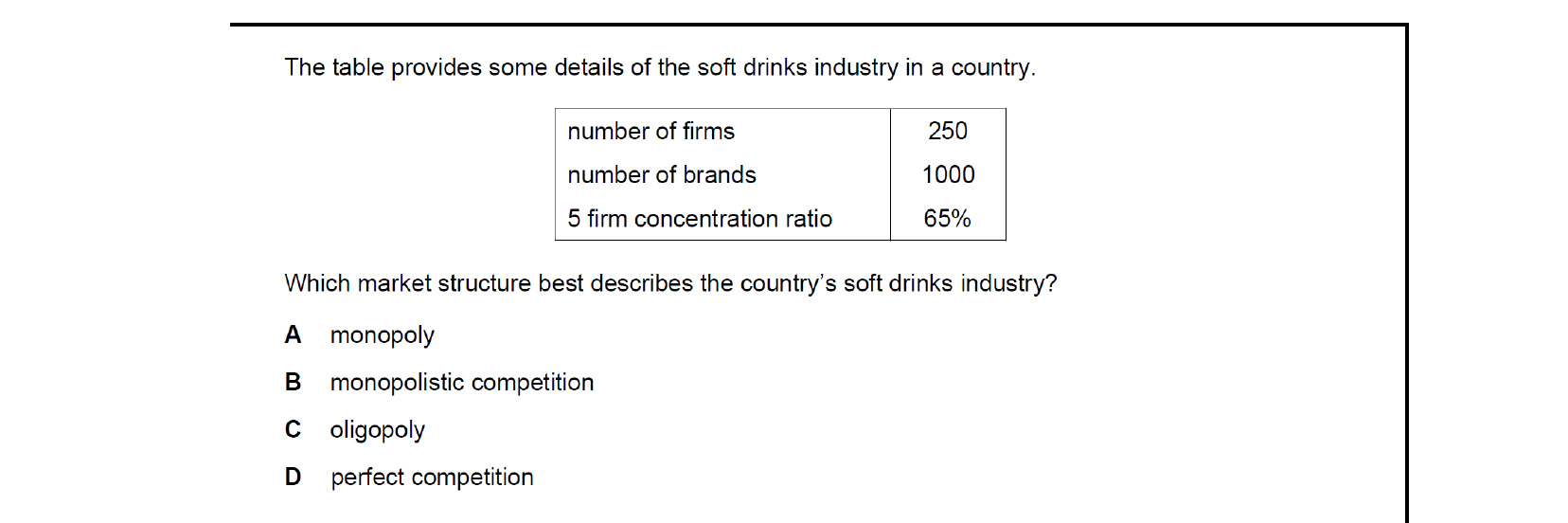

Concentration ratios show the share of the largest few firms. A five-firm ratio of 65% means the top five firms control about two-thirds of output, while many smaller firms supply the rest. That combination of dominant large firms and a competitive fringe is the defining feature of an oligopolistic market, so the structure is oligopoly.

35.2Barriers to entry and exit

Barriers to entry are obstacles that deter or prevent new firms from entering a market to challenge existing producers. Their existence is the dividing line between the more competitive structures (perfect and monopolistic competition) and the less competitive ones (oligopoly and monopoly). Barriers give established firms market power, allowing them to act without the immediate threat of new rivals. New firms will only attempt entry when the expected benefits exceed the cost of breaking through the barriers.

Legal barriers

The economic activity may be state-owned or operated under licence, creating a legal monopoly designed to meet social or political objectives. The economic justification often appeals to natural monopoly — where a single producer is more efficient than several competing ones. A patent is another form of legal barrier: it grants the inventor of a product or process the exclusive right to use it for a fixed period, preventing rivals from copying without permission. Patents are designed to reward original ideas but only for a reasonable period of time.

Market barriers

Advertising and strong brand names with high consumer loyalty are difficult to overcome. Many firms regard advertising as a form of investment because it weakens the substitutability of rival products in consumers' eyes. An existing firm may also saturate the shelves with multiple brands of its own, leaving little space for an entrant. Collaboration between incumbents to develop new products can place the necessary resources beyond the reach of any single new firm. Recessionary market conditions, which leave incumbents with surplus capacity, also deter entry.

Cost barriers

High fixed costs or set-up costs — found in electricity generation, aircraft and car production, and pharmaceuticals — restrict entry to firms that can fund the necessary capital investment. Research and development expenditure forms a large proportion of total costs, and many years of high sales may be needed before a new firm becomes profitable. Economies of scale are themselves a barrier: large incumbents enjoy lower average costs and can cut price to eliminate higher-cost entrants. Predatory pricing is the extreme version, in which a firm sells below average variable cost to force rivals out. Limit pricing is a related tactic: firms deliberately accept a lower price than the profit-maximising one and hide the existence of supernormal profit so that potential entrants see no opportunity worth pursuing. If incumbents agree to do this, it becomes a form of collusion. In fast-moving industries such as consumer electronics, the pace of product innovation is itself a barrier: incumbents are already working on the next generation while launching the current one.

Physical barriers

Some firms control access to raw materials, components or retail outlets, making entry difficult for any rival that lacks the same access. Vertically integrated manufacturers, which control multiple stages of production, gain a cost advantage because rivals must source these stages externally at higher cost.

Barriers to exit

A barrier to exit arises where shutting down would impose costs that cannot be recovered. Research and development outlays, and other resources that cannot easily be redeployed to other uses, are sunk costs. The risk that entry will lead to losses that cannot be recouped on exit is itself a deterrent to entry, so barriers to exit reinforce barriers to entry.

35.3Performance of firms in different market structures

This section moves along the spectrum of competition, from the most competitive structure to the least, comparing each model in terms of prices, revenue, output and profits in both the short and the long run (see Figures 35.6, 35.8, 35.9, 35.12 and 35.13).

Perfect competition

Perfect competition is a theoretical extreme used as a benchmark. Its defining features are a large number of buyers and sellers with perfect knowledge of market conditions, no individual firm having any influence on price (all firms are price takers), a homogeneous product, complete freedom of entry and exit, and full information about products, prices and methods of production. No real-world market matches it exactly, although agriculture and the global market for foreign exchange come closest.

Because the firm cannot influence price, the demand curve facing the individual firm is perfectly elastic at the ruling market price. Marginal revenue equals average revenue equals price, so all of the firm's revenue information lies on the single horizontal line D = AR = MR. The only decision the firm makes is the level of output. A profit-maximising firm produces where MC = MR, since at that output the revenue from the last unit equals its cost.

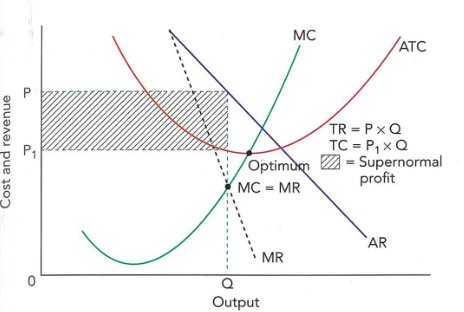

Total revenue is price multiplied by quantity. If total cost is below total revenue, the firm earns supernormal profit; if TC equals TR, the firm earns normal profit. If costs exceed revenue but price still covers average variable cost (AVC), the firm continues in the short run, losing an amount equal to its fixed costs — this minimum price is the shut-down price. Below the minimum AVC, the firm produces nothing because any output would deepen the loss beyond fixed costs. Because the firm produces wherever MC = MR (Price), the portion of the MC curve above the minimum of AVC is the firm's short-run supply curve.

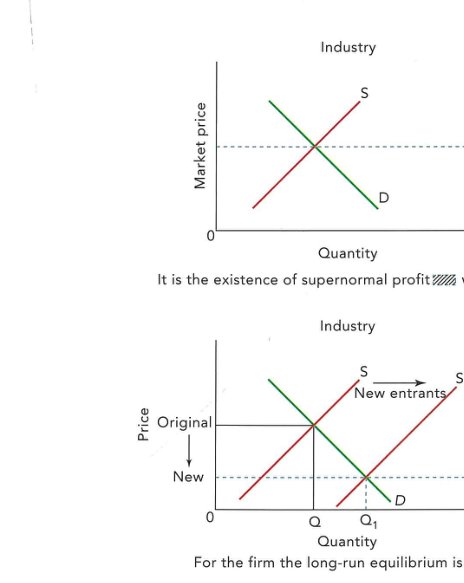

In the long run, the absence of barriers to entry means that supernormal profit attracts new firms. Market supply rises, the price falls, and supernormal profit is competed away. If long-run losses persist, firms leave the market, supply contracts and price rises until the survivors at least cover all costs. The long-run equilibrium is therefore where the most efficient firms produce at minimum average cost and earn normal profit. They are both productively efficient (producing at minimum ATC) and allocatively efficient (P = MC). This is what makes the model a benchmark for criticising less competitive structures.

Key concept link — Efficiency and inefficiency

The model of perfect competition is the most efficient market structure in the long run. All other market structures are inefficient to varying degrees in terms of their output, prices and profits.

Monopolistic competition

Monopolistic competition is the model closest to perfect competition because of the large number of competing firms. Its characteristics are: many buyers and sellers; few barriers to entry and easy exit (capital expenditure can largely be recouped); a wide choice of differentiated products, with each firm enjoying a slight degree of monopoly power over its own brand; and limited influence on price, making firms price makers within a narrow band.

Each firm faces a downward-sloping demand curve, but it is relatively elastic because close substitutes exist. The firm may cut price to expand revenue. As in perfect competition, supernormal profit is possible in the short run but the freedom of entry erodes it. In the long run profit-maximising firms can only earn normal profit.

The behaviour of firms in this structure revolves around product differentiation. A strong brand image is built through advertising and promotion, which not only shifts the firm's demand curve to the right at rivals' expense but also reduces the price elasticity of demand by making consumers see fewer close substitutes. This is brand loyalty. However, advertising is used by all rivals, which can simply raise everyone's costs without yielding lasting advantage. Successful advertisers may move their consumers onto the inelastic portion of the demand curve, where higher prices raise total revenue.

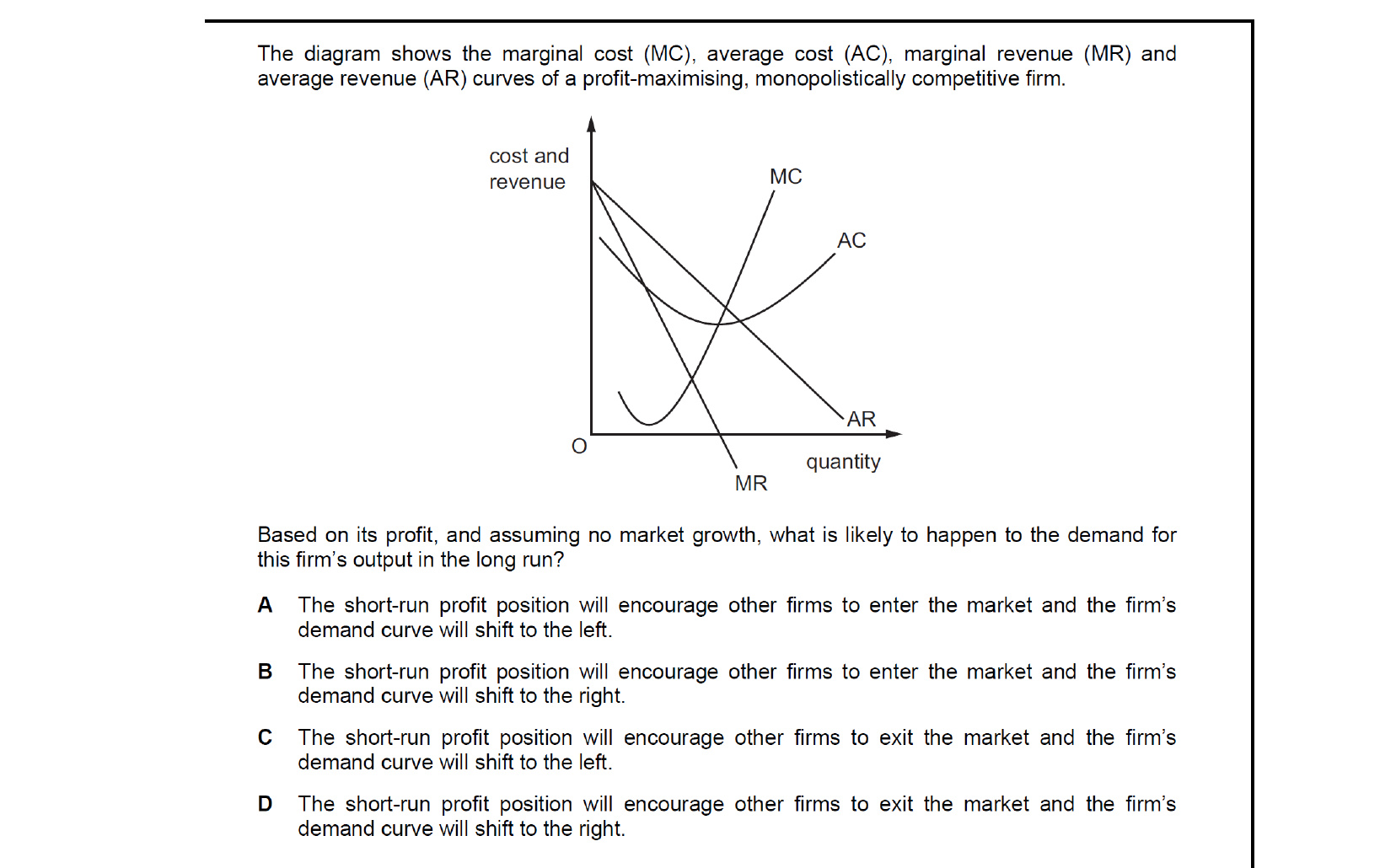

In the short run a profit-maximising firm makes supernormal profit. Over time, entry by new firms shifts each firm's demand curve to the left until only normal profit remains. A key point is that in both the short and the long run the firm is inefficient: it produces above the minimum point of its ATC curve, leaving excess capacity, and it is allocatively inefficient because P > MC. Typical examples include take-away food outlets, local restaurants, garage repair shops, market stalls, builders and travel agents.

Oligopoly

Oligopoly is a market dominated by a few firms. Although the theory does not deliver the single, definite price and output prediction of the other models, oligopoly is possibly the most realistic description of many real industries. Its main features are: dominance by a few firms; interdependence — each firm must anticipate the reactions of its rivals; high or substantial barriers to entry; products that may be differentiated or undifferentiated; and a tendency to price rigidity because of the uncertainty surrounding price competition.

A concentration ratio is used to measure the market power of firms in an oligopoly. The value of sales is the usual basis but physical output or employment can also be used. There is no fixed rule, but a four-firm concentration ratio above 60% is generally described as 'highly oligopolistic'.

The kinked demand curve

The traditional model of oligopoly is the kinked demand curve. It assumes firms are interdependent but there is no collusion. If a firm raises its price, rivals do not follow because they have nothing to gain, so the firm loses sales: demand above the current price is relatively elastic. If the firm lowers its price, rivals follow to defend their market share, so the firm gains few extra sales: demand below the current price is relatively inelastic. The firm's best position is at the kink, with price P and output Q. Even if marginal costs change between two limits, the firm has no incentive to alter price, which gives price rigidity in oligopolistic markets.

Many economists now question the model. It is criticised because the location of the kink is chosen arbitrarily — the model provides no explanation of where price and output start from — and because in many real oligopolies price competition is in fact intense, especially when new entrants are threatening market share.

Non-price competition

Because price competition is risky, oligopolists often prefer non-price competition. This includes advertising and promotions, product innovation (making the product more appealing), brand proliferation (saturating the market with multiple brands so rivals find no gap), market segmentation (adapting the product to particular consumer groups) and process innovation (cutting average costs so price can be reduced without sacrificing profits). The difficulty of predicting rivals' reactions can shift the firm's objective away from profit maximisation towards maintaining market share or earning just enough profit to satisfy shareholders.

The Prisoner's Dilemma in oligopolistic markets

The Prisoner's Dilemma illustrates why two otherwise rational players may fail to cooperate. Two suspects in a crime are interrogated separately and can either stay silent or betray the other. The pay-off matrix is structured so that each suspect's individually best response is to betray, even though both would do better by both staying silent. Applied to a cartel, each member has an incentive to break ranks and produce more than its quota; if all do so, the cartel collapses and consumers may ultimately benefit from cheaper supplies.

Collusion in oligopolistic markets

When firms find it in their interest to cooperate, they may pool research and development costs in joint ventures — common when technology changes rapidly. Collusion proper is the opposite: an anti-competitive action by producers. Informal collusion often takes the form of price leadership, in which firms follow the price chosen by the dominant firm, jointly behaving as a single seller and maximising group profit. A cartel is a formal price or output agreement between firms; this is illegal in most jurisdictions. In practice it is difficult to identify either formal or informal collusion because aggressive price competition can produce similar price patterns, which makes anti-competitive investigations time-consuming and often inconclusive.

Monopoly

A pure monopoly is a single firm controlling the whole industry. The term is also used where one firm has a very large share — in some jurisdictions, a firm with more than 25% of the market is treated as a legal monopoly. Monopoly's defining features are a single seller, no close substitutes, high barriers to entry, and a price-making firm. Monopoly need not mean a giant corporation: small local monopolies can exist where it is unprofitable for others to enter.

A pure monopolist faces the market demand curve, which slopes downward. The firm decides on either price or quantity but not both. A profit-maximising monopolist produces where MC = MR, sells at the price consumers are willing to pay on the demand curve at that quantity, and earns supernormal profit if total revenue exceeds total cost. In monopoly there is no distinction between the short run and the long run, because barriers to entry prevent supernormal profit from being competed away — there is no economic incentive for the monopolist to move from the profit-maximising output. Where fixed costs are so high that the price consumers can afford only covers production costs, the monopolist may earn only normal profit despite its market power. A monopolist can also use price discrimination — selling the same product at different prices to different customers — to increase profit.

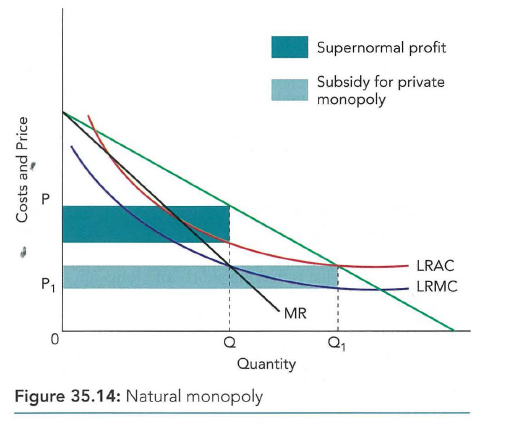

Natural monopoly

A natural monopoly arises where one firm has an overwhelming cost advantage. Long-run average costs fall continuously over the relevant range of output because fixed costs are a very high percentage of total costs, so spreading them over more output keeps reducing average cost. Duplicating the network would be wasteful. Typical examples are water, gas, electricity, railways and inland waterways. A profit-maximising natural monopoly sets price P and output Q and earns supernormal profit; if instead it priced at long-run marginal cost (P = LRMC), price would be lower at P1 and quantity higher at Q1, but the firm would make a loss because LRMC lies below LRAC. This is sustainable only if the government subsidises the firm on the grounds that the service is essential, or if the service is provided by the public sector with internal cross-funding of losses.

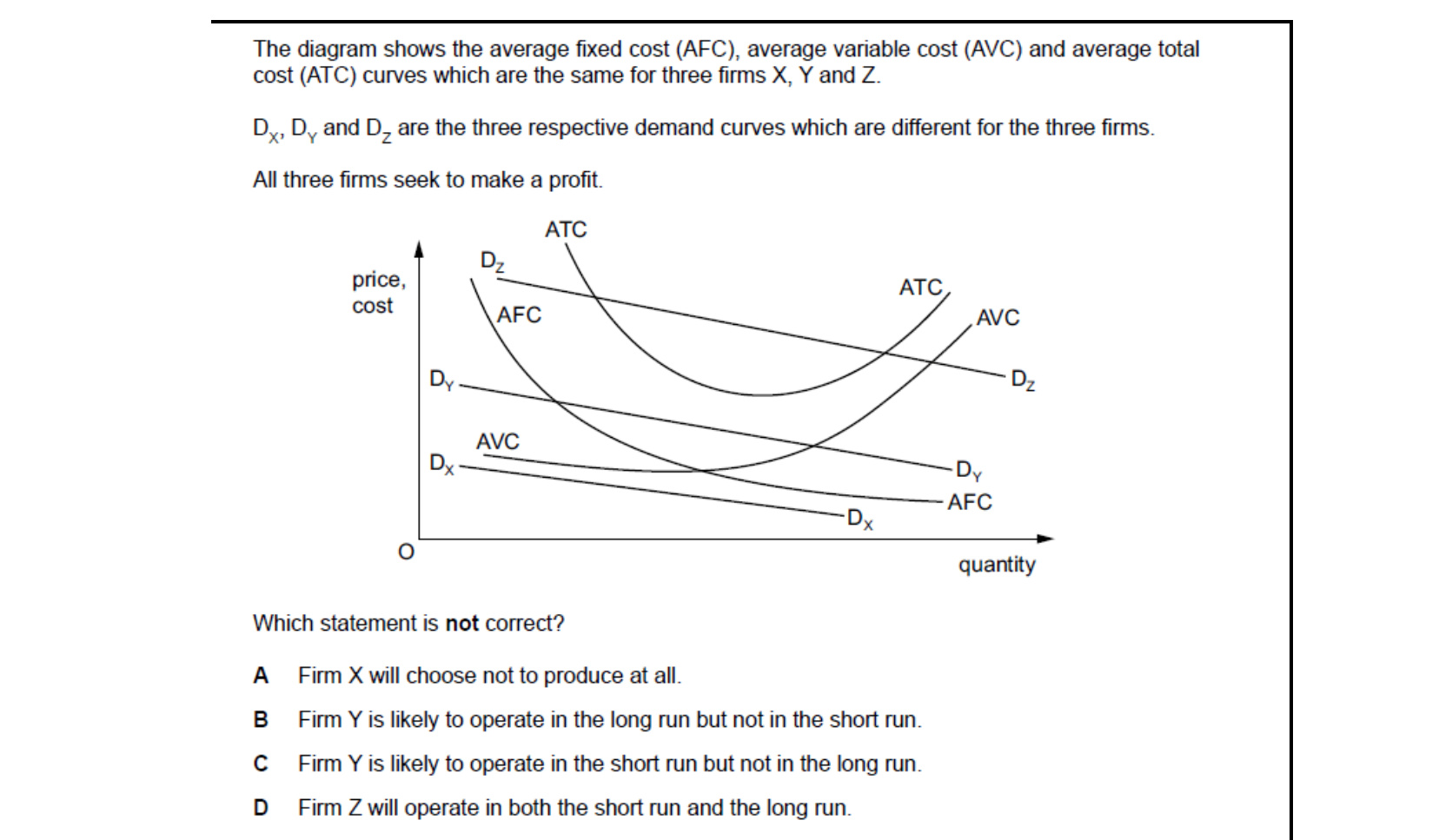

Firm X's demand lies entirely below AVC, so it cannot cover variable cost and will not produce. Firm Y's demand lies between AVC and ATC, so it covers variable cost (operates in SR) but not total cost (exits in LR). Firm Z's demand lies above ATC, so it covers all costs and operates in both periods. The incorrect statement therefore is that Y will operate in the long run but not the short run.

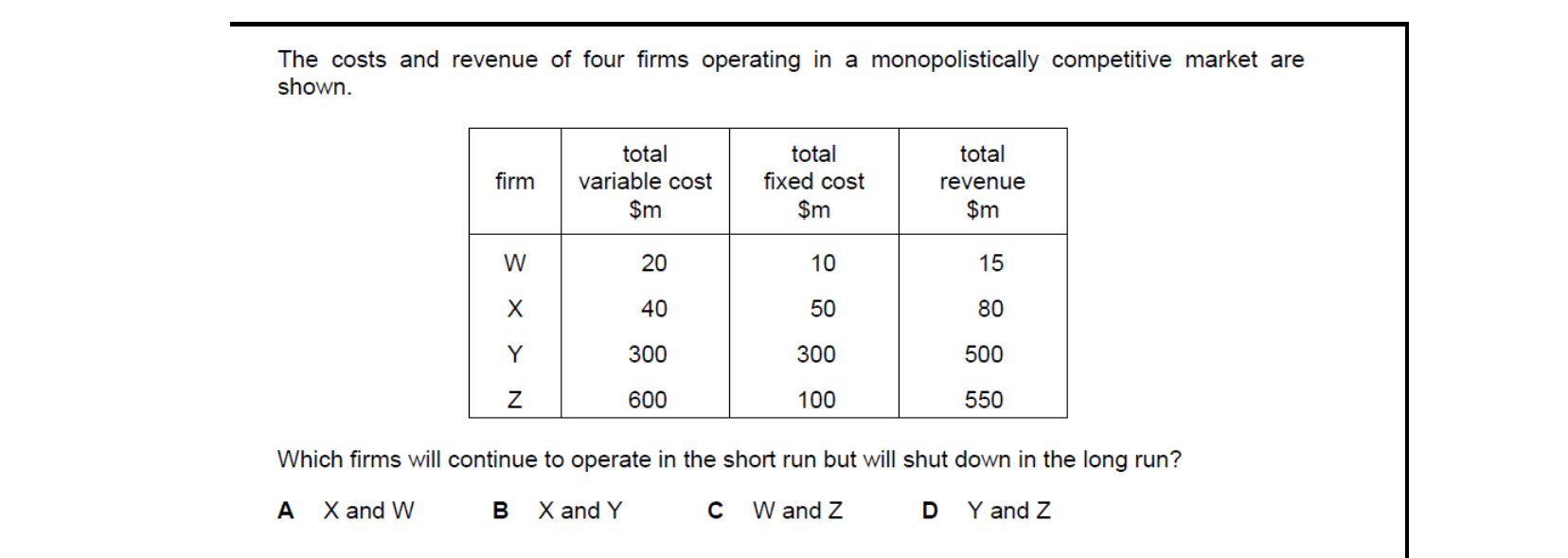

In the short run a firm continues if total revenue covers total variable cost. In the long run it must also cover fixed cost (TR >= TC). Checking each firm: W (TR 35, TVC 20, TFC 10 -> covers TVC and TC, stays). X (TR 80, TVC 40, TC 90 -> covers TVC but not TC, stays SR, exits LR). Y (TR 500, TVC 300, TC 600 -> covers TVC but not TC, stays SR, exits LR). Z (TR 550, TVC 600 -> does not cover even TVC, shuts immediately). So firms X and Y continue in the SR but shut in the LR.

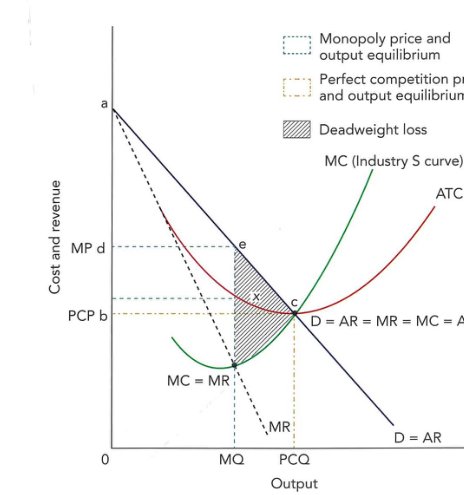

35.4Comparison of monopoly with perfect competition

The classic case against monopoly is that its conduct and performance compare unfavourably with firms in more competitive markets. A diagram setting the equilibrium of a profit-maximising single-price monopolist alongside that of a perfectly competitive industry brings out the differences clearly. The relevant observations are: (see Figures 35.15 and 35.16)

- The price under monopoly (MP) is higher than the price under perfect competition (PC).

- The output under monopoly (MQ) is lower than the output under perfect competition (PCQ).

- The monopolist makes both short-run and long-run supernormal profit, because barriers to entry prevent new firms from competing it away.

- The firm in perfect competition is productively efficient, producing at the minimum point of its ATC, and allocatively efficient, producing where P = MC.

- The monopolist captures consumer surplus and converts it into supernormal profit.

- The monopolist is productively inefficient (producing below the optimum output) and allocatively inefficient (price is well above marginal cost).

If a perfectly competitive industry were turned into a monopoly, the result would be a welfare loss as well as greater allocative inefficiency. Three further inefficiencies follow from the comparison of the two equilibria. Consumer surplus in monopoly is less than in perfect competition because of the higher price. Producer surplus in monopoly is greater than in perfect competition because the monopolist's higher price and lower output have taken away some of what was previously enjoyed by consumers. The deadweight loss is the sum of consumer surplus and producer surplus that disappears when the industry moves to monopoly. It is significant because the monopolist gains at the expense of consumers by converting some of the consumer surplus into producer surplus.

Qualifying the criticism

The criticism of real-world monopolies based on a comparison with perfect competition may not be wholly valid for two reasons. First, perfect competition is a theoretical ideal. To have more relevance, monopoly should be compared with the more realistic models of monopolistic competition and oligopoly. These structures are themselves characterised by productive and allocative inefficiency, and they may also involve wasteful expenditure on competitive advertising. Second, the standard comparison assumes the same costs in monopoly as in perfect competition. This ignores the possibility that the monopolist can achieve internal economies of scale that would reduce unit costs. In that case the monopoly price could in principle be lower than the competitive price, leaving consumers better off even though the monopolist is making supernormal profit.

The positive case for monopoly

Several arguments can be made in favour of monopoly in particular circumstances.

- Supernormal profit is not guaranteed. A monopolist cannot always make supernormal profit - it depends on the level of its costs. Where fixed costs are very large relative to total cost, the market price may only just cover average cost, leaving the monopolist with normal profit.

- Stable profits support long-term planning. A competitive market is criticised for the uncertainty of profits in the long run. A monopolist can plan future investment and finance it through guaranteed profits, which may deliver better products and greater security for the workforce.

- Innovation. Investment funded by supernormal profit may take the form of process innovation, applying new techniques of production with the objective of lowering unit costs. Alternatively, profit can fund product innovation, which adds to consumer welfare by improving performance or widening consumer choice.

- Pass-through to consumers. If the benefits of economies of scale and greater investment are passed on, it can be argued that consumers gain from the existence of supernormal profit.

X-inefficiency

A common criticism of state-owned monopolies in particular is that the absence of competition makes them less efficient. The argument is that firms with a guaranteed market can be complacent. Monopolies are said to suffer from X-inefficiency, a form of productive inefficiency. X-inefficiency means that a firm is not producing at the lowest possible cost for a given level of output. The monopolist's cost levels are higher than they would be in a competitive firm. Monopolists do not have the same control over costs: there may be too many workers, or capital may not be used efficiently. Some investment may also take the form of erecting barriers to maintain supernormal profit, which adds to costs in the short run and is at the expense of efficiency. The actual LRAC curve therefore sits above the potential LRAC curve a more competitive firm could achieve, with the gap representing X-inefficiency. There is always the possibility that these inefficiencies are outweighed by the benefits of economies of scale that lower average costs.

It is clear that monopolies can operate in ways that lead to inefficiency or consumer exploitation. However, it is also possible to make a positive case for monopoly. This explains why investigating monopoly practices is difficult and why each case must be judged on its own merits. Monopoly should not be assumed to be always harmful; the performance of a monopolist may be little different from that of firms in oligopolistic markets.

Vaccine production is dominated by a few large pharmaceutical firms with patents and high R&D costs, so the market is imperfectly competitive rather than perfectly competitive. Each vaccination also benefits third parties through herd immunity, which is a positive consumption externality. The correct pairing is therefore imperfect competition and positive consumption externality.

35.5Contestable markets

The market structure models considered so far - perfect competition, monopolistic competition, oligopoly and monopoly - have all been analysed in turn. A contestable market is not on that list. This is because, although contestability increasingly features in many markets, a contestable market is not a market structure as such. It is best seen as a set of conditions that can apply within any of the three imperfectly competitive structures (monopolistic competition, oligopoly or monopoly).

The concept of contestability was developed by the economist William Baumol, originally in the context of domestic air transport. Baumol argued that if a market was contestable rather than heavily regulated, fares would fall because of the threat of new airlines entering. An important consideration was that airlines leased their planes, meaning there were few costs to bear when the planes were handed back on exit. When these ideas were implemented by deregulating the domestic airline market, new firms entered quickly, fares fell on routes facing new competition and new services emerged. The experience proved particularly significant for governments implementing policies of deregulation and privatisation, which incorporated provisions for contestability into former public-sector industries. Many other economies have since applied similar policies to make their markets more competitive. The application of contestability to global air transport is now widespread, with 'open skies' policies the norm; market demand has grown, particularly for short-haul services provided by low-cost carriers operating from smaller airports. The business is not risk-free - many firms have been forced out - but contestability disciplines those that remain.

What makes a market contestable

A market is contestable if potential competitors can influence the conduct of existing firms in the market. Potential competitors include similar firms not currently operating in the market, or new firms that could set up if they saw an opportunity to gain market share and operate successfully. What potential entrants must assess is whether the likely gains from market entry exceed the costs of entry. Barriers to entry and to exit are therefore crucial in determining whether a market is really contestable.

According to the concept, a perfectly contestable market is one where entry and exit are free or costless. This must be the case if potential competitors are not to be at a relative disadvantage compared with firms already in the market. If entry is not free, new firms will experience higher costs, suffer from a lack of access to technology and be unable to compete effectively because of the brand loyalty that has been built up by firms already in the market. The fewer the barriers to entry and the lower the cost of entry, the more contestable the market will be.

Exit must also be costless. This means that in a perfectly contestable market, firms will have no sunk costs - when they leave the market, they can resell any assets they have used without loss. If this were not possible, potential entrants might be put off from entering a market. Sunk costs would therefore be seen as a barrier to entry.

The result of costless entry and exit is that contestable markets are characterised by what is known as 'hit and run' entry. A typical example would be the case of a firm attracted to enter a market by the high level of profits being earned by existing firms. On entry, the firm would take a share of the profits but then leave once profit levels fell back to normal. In this way, firms are not able to earn supernormal profit in the long run. Contestability describes how close a real market is to these ideal conditions. Deregulation - the removal of legal and regulatory barriers to entry - is one way governments can raise contestability.

The conditions for a perfectly contestable market

A market is perfectly contestable where:

- there is a pool of potential entrants seeking to enter the market;

- entry and exit are costless;

- all firms are subject to the same regulations and state of technology;

- mechanisms are in place to prohibit limit pricing, as existing firms have lower costs than potential entrants;

- firms already in the market are vulnerable to 'hit and run' competition.

In theory, as long as entry is free and exit is costless, any market structure could meet the requirements of a perfectly contestable market.

Contestability across the structures

Each imperfect structure has different starting conditions for contestability:

- Monopolistic competition already has few barriers to entry. Because of non-price competition, it takes small firms time to build a customer base and to obtain brand loyalty. There are still barriers in the form of licensing requirements and other regulatory hurdles.

- Oligopolistic markets have high barriers to entry, particularly in the form of the capital costs of entry and the expenditure needed to build up market share.

- Monopoly power obtained through a patent or legal right to operate in a market leaves the market wholly uncontestable. In other monopoly situations, however, there could be an opportunity for new firms to enter, although the cost of entry will certainly not be zero.

In each of these market structures there could be a high degree of contestability depending on the costs of entry into and exit from the market. In a contestable monopoly with no barriers, a new entrant attracted by the incumbent's supernormal profit forces the monopolist to reduce price to the level at which average cost equals average revenue. The monopolist is now producing the same level of output but selling at the lower price in order to maximise the volume of sales; only normal profit is earned because average cost equals average revenue.

In theory, a perfectly competitive market is most similar to a perfectly contestable market because in both there are no barriers to entry or exit. In a perfectly contestable market:

- only normal profits are earned in the long run;

- firms are not able to apply cross-subsidisation;

- prices cannot be set below average cost to deter new entrants;

- allocative efficiency and productive efficiency are being achieved;

- the number of firms in the market does not matter.

Key concept link - Efficiency and inefficiency

The underpinning rationale for contestability in markets is that of efficiency. By opening up markets to competition, and having a situation where market entry is easy for new firms, this puts continual pressure on firms already in the market to be more efficient. Any hint of supernormal profit being made should be a signal for the entry of new firms.

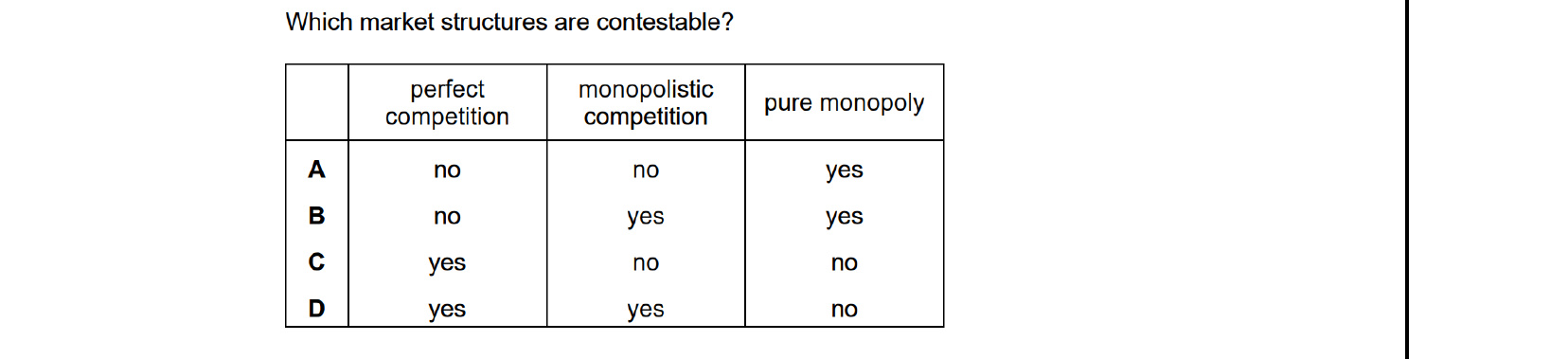

A contestable market is one with free entry and costless exit, so incumbents are disciplined by the threat of new entrants. Perfect competition has costless entry, and monopolistic competition also has very low barriers to entry, so both are contestable. Pure monopoly is by definition protected by high barriers to entry, so it is not contestable. The correct row is therefore yes/yes/no.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

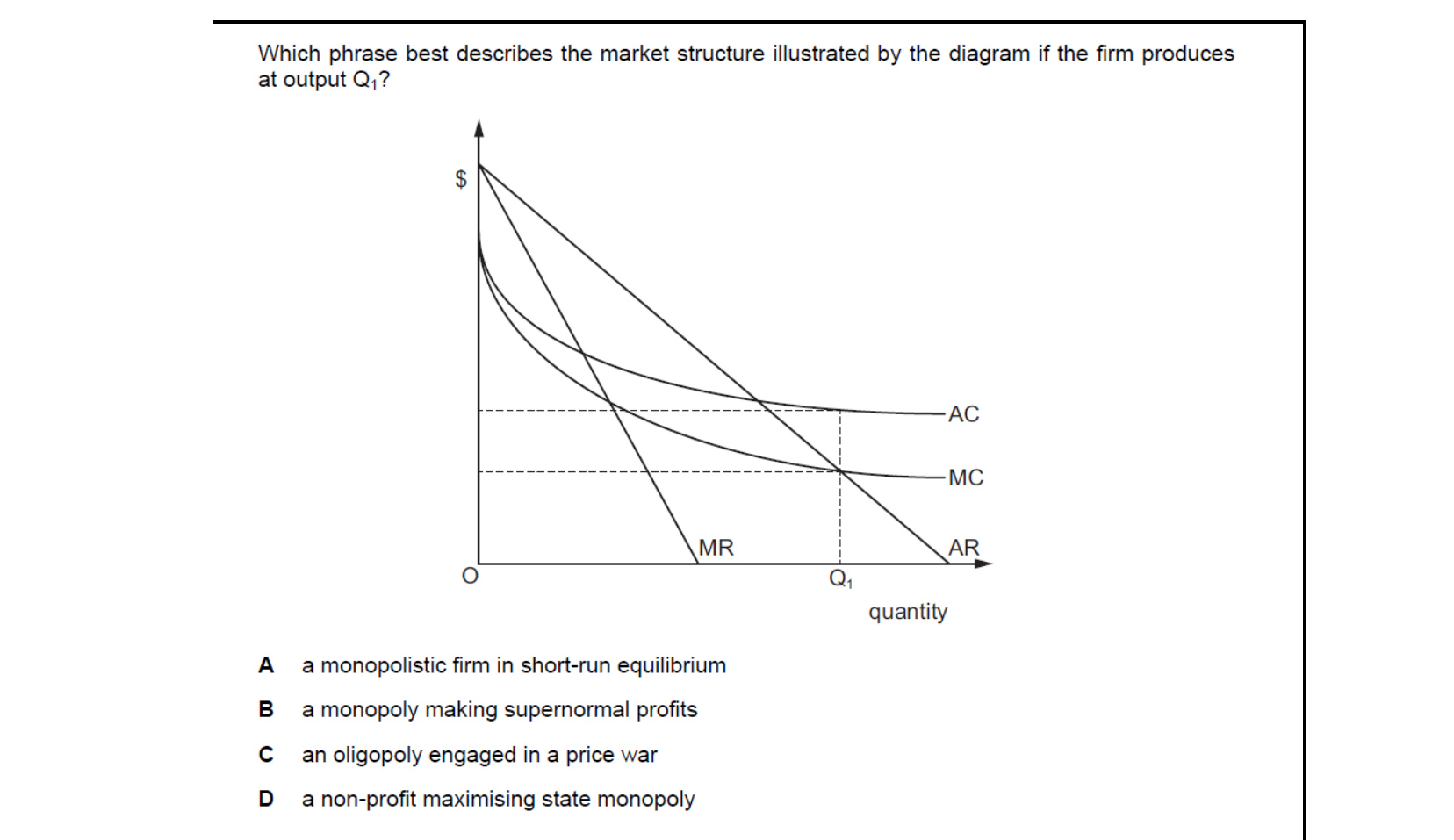

The diagram shows MC cutting MR above AR but the firm producing at Q1 - well below the profit-maximising MC = MR output - with no supernormal profit being maximised. This pattern (deliberately producing more than the profit-maximising level for political or social reasons) is typical of a non-profit-maximising state monopoly.

A cartel only works if every member sticks to the agreed prices or output quotas. Any single member can gain by cheating - producing more to undercut the cartel price - but if any member breaks rank the agreement collapses. Effective operation therefore requires full cooperation: every member must keep to the agreement.

If firms leave the industry, total industry supply falls. The market supply curve - the horizontal sum of individual firm supply curves - shifts to the left, so less is supplied at any given price. A movement along the supply curve would require a price change, not an exit, so the correct effect is a leftward shift of the supply curve.

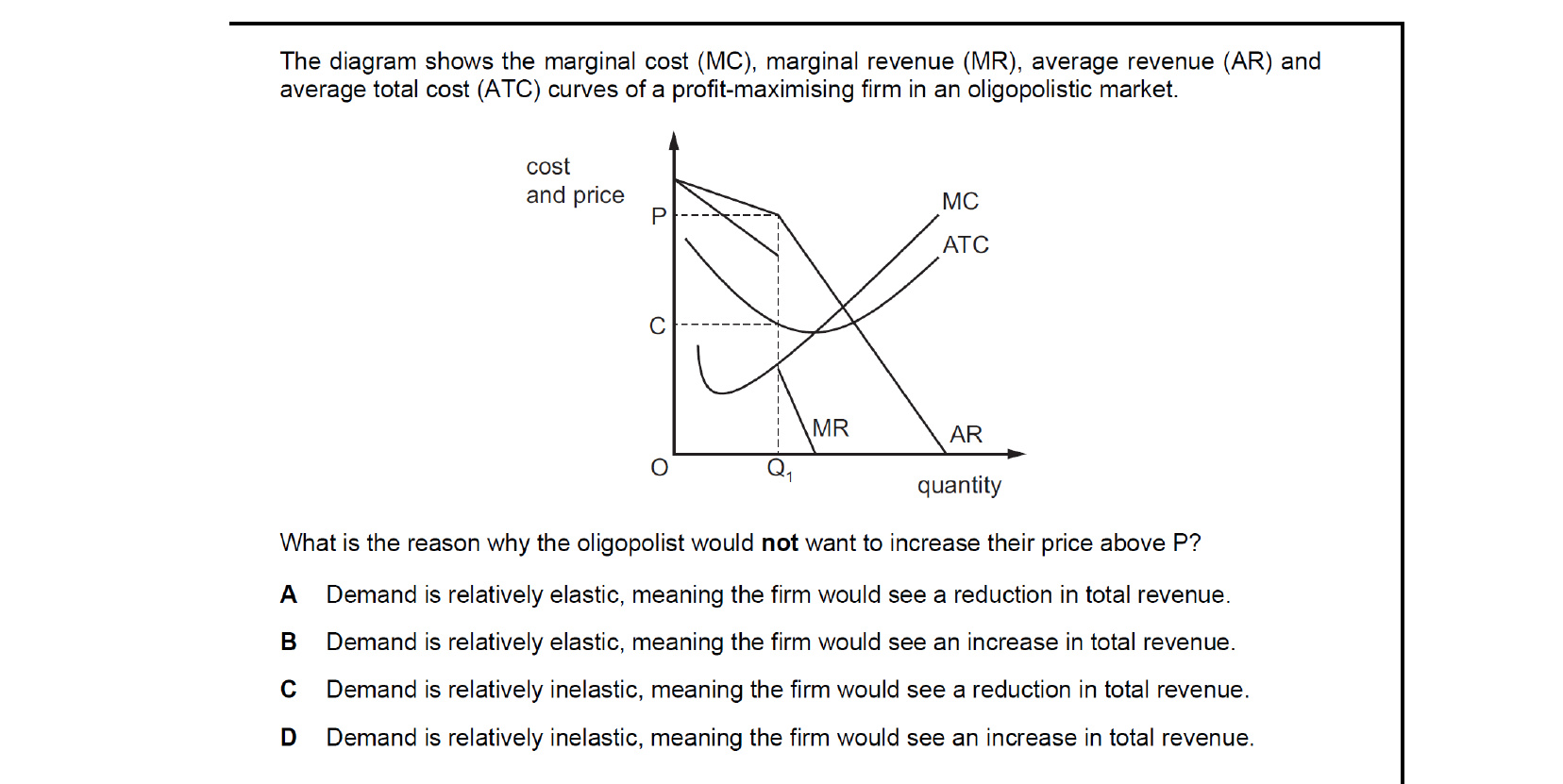

The diagram shows the kinked demand curve typical of oligopoly. Above the current price P, demand is relatively elastic because rivals will not follow a price rise, so the firm would lose customers and total revenue would fall. This is why the oligopolist does not increase price above P - demand is relatively elastic and total revenue would fall.

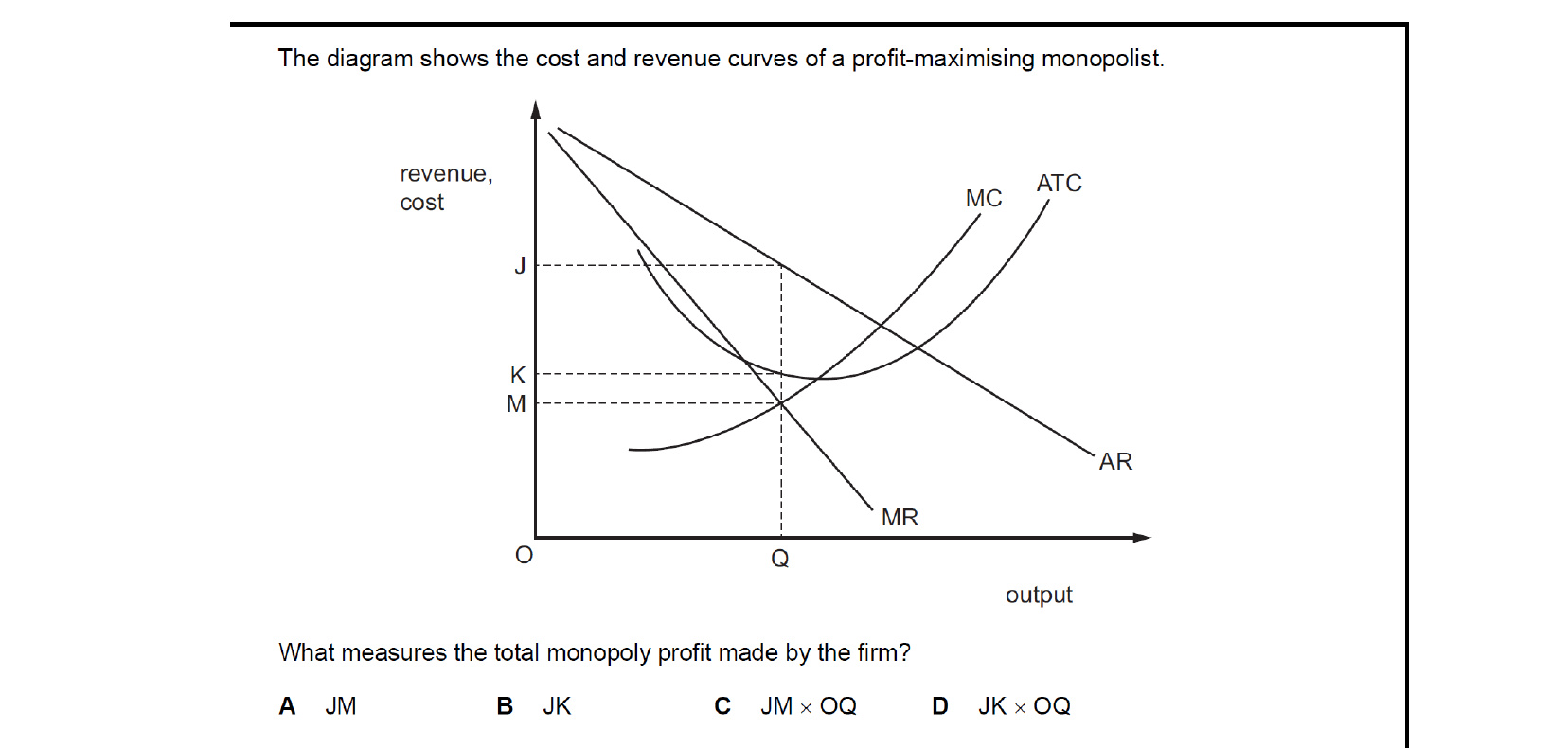

Monopoly profit per unit equals AR minus ATC at the profit-maximising output Q. From the diagram AR at Q is J and ATC at Q is K, so profit per unit is JK. Total profit equals profit per unit times quantity, so total monopoly profit is JK times OQ.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Describe the features of the market structures of perfect competition, monopoly, monopolistic competition, oligopoly and natural monopoly.

- Explain the characteristics of market structures through the number of buyers and sellers, product differentiation, freedom of entry and exit, and availability of information.

- Explain barriers to entry (legal, market, cost, physical) to and exit from an industry.

- Analyse the performance of firms in different market structures in terms of their relative efficiency as determined by prices, revenue, output and profits in the short run and in the long run.

- Explain and calculate a concentration ratio to measure the power of firms in a market.

- Consider the relevance of the Prisoner's Dilemma in oligopolistic markets.

- Explain the purpose of collusion in oligopolistic markets.

- Compare monopoly with perfect competition and consider X-inefficiency in the short run and the long run.

- Analyse the characteristics of contestable markets.

Want more practice? Drill this chapter's past-paper MCQs (131 questions) →